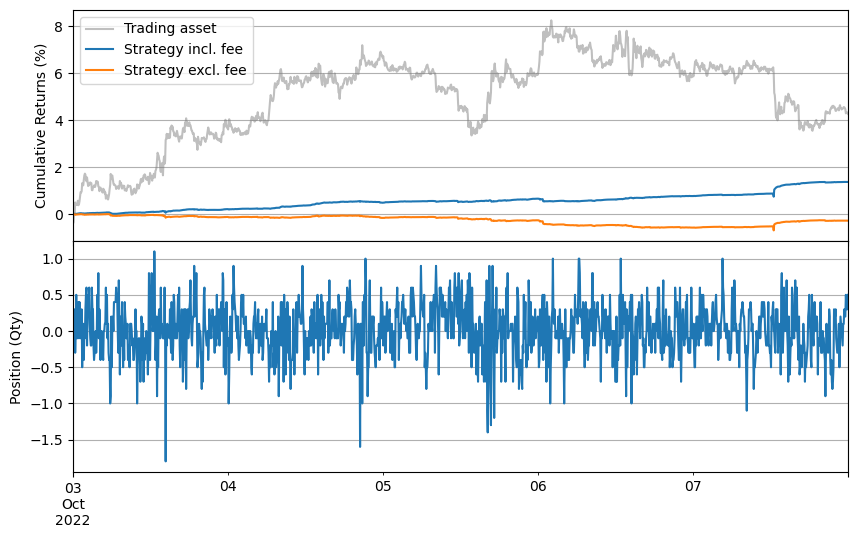

High-Frequency Grid Trading

Note: This example is for educational purposes only and demonstrates effective strategies for high-frequency market-making schemes. All backtests are based on a 0.005% rebate, the highest market maker rebate available on Binance Futures. See Binance Upgrades USDⓢ-Margined Futures Liquidity Provider Program for more details.

Plain High-Frequency Grid Trading

This is a high-frequency version of Grid Trading that keeps posting orders on grids centered around the mid-price, maintaining a fixed interval and a set number of grids.

[1]:

from numba import njit

import pandas as pd

import numpy as np

from numba.typed import Dict

from hftbacktest import NONE, NEW, HftBacktest, GTX, FeedLatency, SquareProbQueueModel, BUY, SELL, Linear, Stat, reset

@njit

def gridtrading(hbt, stat):

max_position = 5

grid_interval = hbt.tick_size * 10

grid_num = 20

half_spread = hbt.tick_size * 20

# Running interval in microseconds

while hbt.elapse(100_000):

# Clears cancelled, filled or expired orders.

hbt.clear_inactive_orders()

mid_price = (hbt.best_bid + hbt.best_ask) / 2.0

bid_order_begin = np.floor((mid_price - half_spread) / grid_interval) * grid_interval

ask_order_begin = np.ceil((mid_price + half_spread) / grid_interval) * grid_interval

order_qty = 0.1

last_order_id = -1

# Creates a new grid for buy orders.

new_bid_orders = Dict.empty(np.int64, np.float64)

if hbt.position < max_position:

for i in range(grid_num):

bid_order_begin -= i * grid_interval

bid_order_tick = round(bid_order_begin / hbt.tick_size)

# Do not post buy orders above the best bid.

if bid_order_tick > hbt.best_bid_tick:

continue

# order price in tick is used as order id.

new_bid_orders[bid_order_tick] = bid_order_begin

for order in hbt.orders.values():

# Cancels if an order is not in the new grid.

if order.side == BUY and order.cancellable and order.order_id not in new_bid_orders:

hbt.cancel(order.order_id)

last_order_id = order.order_id

for order_id, order_price in new_bid_orders.items():

# Posts an order if it doesn't exist.

if order_id not in hbt.orders:

hbt.submit_buy_order(order_id, order_price, order_qty, GTX)

last_order_id = order_id

# Creates a new grid for sell orders.

new_ask_orders = Dict.empty(np.int64, np.float64)

if hbt.position > -max_position:

for i in range(grid_num):

ask_order_begin += i * grid_interval

ask_order_tick = round(ask_order_begin / hbt.tick_size)

# Do not post sell orders below the best ask.

if ask_order_tick < hbt.best_ask_tick:

continue

# order price in tick is used as order id.

new_ask_orders[ask_order_tick] = ask_order_begin

for order in hbt.orders.values():

# Cancels if an order is not in the new grid.

if order.side == SELL and order.cancellable and order.order_id not in new_ask_orders:

hbt.cancel(order.order_id)

last_order_id = order.order_id

for order_id, order_price in new_ask_orders.items():

# Posts an order if it doesn't exist.

if order_id not in hbt.orders:

hbt.submit_sell_order(order_id, order_price, order_qty, GTX)

last_order_id = order_id

# All order requests are considered to be requested at the same time.

# Waits until one of the order responses is received.

if last_order_id >= 0:

if not hbt.wait_order_response(last_order_id):

return False

# Records the current state for stat calculation.

stat.record(hbt)

return True

[2]:

hbt = HftBacktest(

[

'data/ethusdt_20221003.npz',

'data/ethusdt_20221004.npz',

'data/ethusdt_20221005.npz',

'data/ethusdt_20221006.npz',

'data/ethusdt_20221007.npz'

],

tick_size=0.01,

lot_size=0.001,

maker_fee=-0.00005,

taker_fee=0.0007,

order_latency=FeedLatency(),

queue_model=SquareProbQueueModel(),

asset_type=Linear,

snapshot='data/ethusdt_20221002_eod.npz'

)

stat = Stat(hbt)

Load data/ethusdt_20221003.npz

[3]:

%%time

gridtrading(hbt, stat.recorder)

Load data/ethusdt_20221004.npz

Load data/ethusdt_20221005.npz

Load data/ethusdt_20221006.npz

Load data/ethusdt_20221007.npz

CPU times: user 3min 58s, sys: 6.03 s, total: 4min 4s

Wall time: 4min 5s

[3]:

True

[4]:

stat.summary(capital=15_000)

=========== Summary ===========

Sharpe ratio: 20.9

Sortino ratio: 22.4

Risk return ratio: 211.5

Annualised return: 330.53 %

Max. draw down: 1.56 %

The number of trades per day: 5954

Avg. daily trading volume: 595

Avg. daily trading amount: 798115

Max leverage: 0.52

Median leverage: 0.21

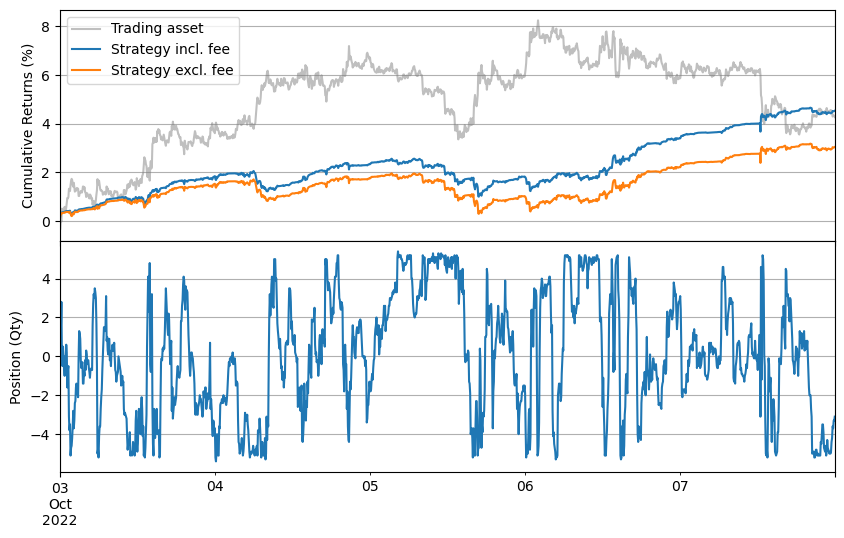

High-Frequency Grid Trading with Skewing

By incorporating position-based skewing, the strategy’s risk-adjusted returns can be improved.

[5]:

@njit

def gridtrading(hbt, stat, skew):

max_position = 5

grid_interval = hbt.tick_size * 10

grid_num = 20

half_spread = hbt.tick_size * 20

# Running interval in microseconds

while hbt.elapse(100_000):

# Clears cancelled, filled or expired orders.

hbt.clear_inactive_orders()

mid_price = (hbt.best_bid + hbt.best_ask) / 2.0

reservation_price = mid_price - skew * hbt.position * hbt.tick_size

bid_order_begin = np.floor((reservation_price - half_spread) / grid_interval) * grid_interval

ask_order_begin = np.ceil((reservation_price + half_spread) / grid_interval) * grid_interval

order_qty = 0.1 # np.round(notional_order_qty / mid_price / hbt.lot_size) * hbt.lot_size

last_order_id = -1

# Creates a new grid for buy orders.

new_bid_orders = Dict.empty(np.int64, np.float64)

if hbt.position < max_position: # hbt.position * mid_price < max_notional_position

for i in range(grid_num):

bid_order_begin -= i * grid_interval

bid_order_tick = round(bid_order_begin / hbt.tick_size)

# Do not post buy orders above the best bid.

if bid_order_tick > hbt.best_bid_tick:

continue

# order price in tick is used as order id.

new_bid_orders[bid_order_tick] = bid_order_begin

for order in hbt.orders.values():

# Cancels if an order is not in the new grid.

if order.side == BUY and order.cancellable and order.order_id not in new_bid_orders:

hbt.cancel(order.order_id)

last_order_id = order.order_id

for order_id, order_price in new_bid_orders.items():

# Posts an order if it doesn't exist.

if order_id not in hbt.orders:

hbt.submit_buy_order(order_id, order_price, order_qty, GTX)

last_order_id = order_id

# Creates a new grid for sell orders.

new_ask_orders = Dict.empty(np.int64, np.float64)

if hbt.position > -max_position: # hbt.position * mid_price > -max_notional_position

for i in range(grid_num):

ask_order_begin += i * grid_interval

ask_order_tick = round(ask_order_begin / hbt.tick_size)

# Do not post sell orders below the best ask.

if ask_order_tick < hbt.best_ask_tick:

continue

# order price in tick is used as order id.

new_ask_orders[ask_order_tick] = ask_order_begin

for order in hbt.orders.values():

# Cancels if an order is not in the new grid.

if order.side == SELL and order.cancellable and order.order_id not in new_ask_orders:

hbt.cancel(order.order_id)

last_order_id = order.order_id

for order_id, order_price in new_ask_orders.items():

# Posts an order if it doesn't exist.

if order_id not in hbt.orders:

hbt.submit_sell_order(order_id, order_price, order_qty, GTX)

last_order_id = order_id

# All order requests are considered to be requested at the same time.

# Waits until one of the order responses is received.

if last_order_id >= 0:

if not hbt.wait_order_response(last_order_id):

return False

# Records the current state for stat calculation.

stat.record(hbt)

return True

Weak skew

[6]:

reset(

hbt,

[

'data/ethusdt_20221003.npz',

'data/ethusdt_20221004.npz',

'data/ethusdt_20221005.npz',

'data/ethusdt_20221006.npz',

'data/ethusdt_20221007.npz'

],

snapshot='data/ethusdt_20221002_eod.npz'

)

stat = Stat(hbt)

skew = 1

gridtrading(hbt, stat.recorder, skew)

stat.summary(capital=15_000)

Load data/ethusdt_20221003.npz

Load data/ethusdt_20221004.npz

Load data/ethusdt_20221005.npz

Load data/ethusdt_20221006.npz

Load data/ethusdt_20221007.npz

=========== Summary ===========

Sharpe ratio: 18.0

Sortino ratio: 17.5

Risk return ratio: 169.2

Annualised return: 166.77 %

Max. draw down: 0.99 %

The number of trades per day: 6488

Avg. daily trading volume: 648

Avg. daily trading amount: 870207

Max leverage: 0.50

Median leverage: 0.10

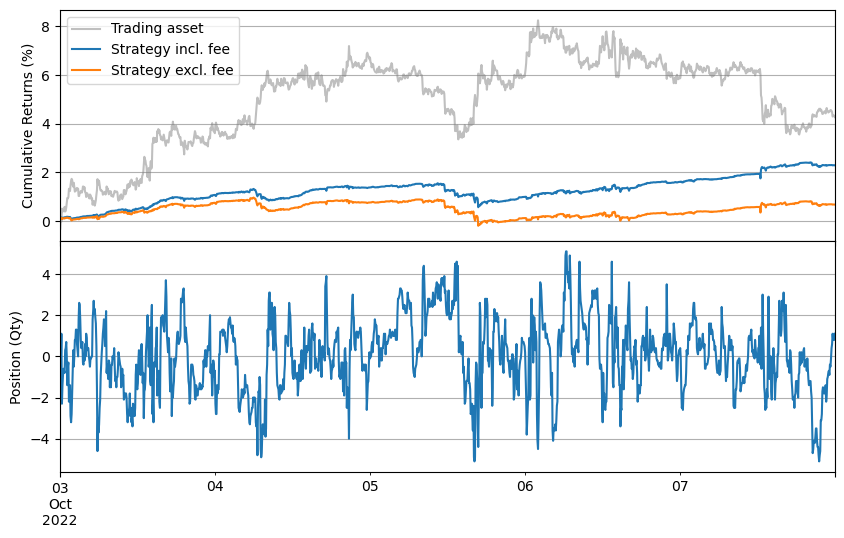

Strong skew

[7]:

reset(

hbt,

[

'data/ethusdt_20221003.npz',

'data/ethusdt_20221004.npz',

'data/ethusdt_20221005.npz',

'data/ethusdt_20221006.npz',

'data/ethusdt_20221007.npz'

],

snapshot='data/ethusdt_20221002_eod.npz'

)

stat = Stat(hbt)

skew = 10

gridtrading(hbt, stat.recorder, skew)

stat.summary(capital=15_000)

Load data/ethusdt_20221003.npz

Load data/ethusdt_20221004.npz

Load data/ethusdt_20221005.npz

Load data/ethusdt_20221006.npz

Load data/ethusdt_20221007.npz

=========== Summary ===========

Sharpe ratio: 29.3

Sortino ratio: 33.4

Risk return ratio: 735.4

Annualised return: 100.30 %

Max. draw down: 0.14 %

The number of trades per day: 6636

Avg. daily trading volume: 663

Avg. daily trading amount: 889749

Max leverage: 0.51

Median leverage: 0.02